Ask any market trader, small business owner, or farmer across Africa about their experience with banks, and you will likely hear the same thing: long queues, high charges, endless paperwork, slow service, and no access to credit when they need it most.

For years, traditional banks have been the go-to, but the truth is, millions are still left out. Especially women-owned businesses, young entrepreneurs, rural communities, and people in the informal sector. Not because they don’t want financial services, but because the system runs on protocols that often leave out the poor, the uneducated, and anyone outside the formal economy.

That’s exactly where fintech is stepping in and offering faster, simpler, and more inclusive financial tools that work for everyday people.

What Is Fintech?

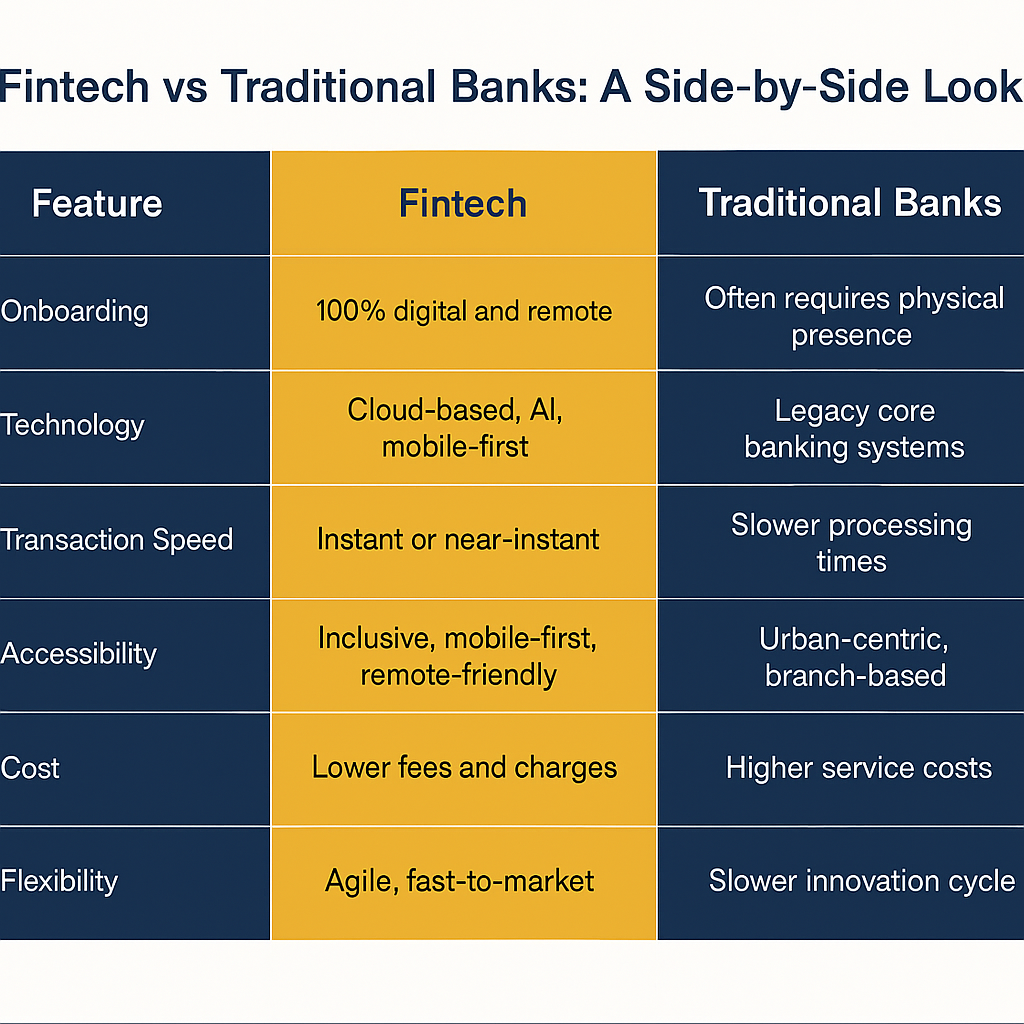

Fintech (financial technology) is simply the use of technology to deliver financial services. That could mean anything from mobile money apps and digital wallets to online savings platforms, payment gateways, peer-to-peer lending, or investment tools. The real value of fintech is in how it simplifies finance. It’s making financial services accessible to more people, especially those who have traditionally been left out of the formal banking system.

The rise of fintech is a response to real problems. For years, people across Africa have faced frustrating banking experiences: long queues, endless paperwork, slow processes, and limited access in rural areas. But fintech changed that; it gave people alternatives. It’s faster, cheaper, and more user-friendly. And when COVID-19 hit, things moved even quicker. In just a few months, mobile banking adoption jumped by 20–50%. People had no choice but to go digital, and many never looked back.

Today, consumers expect speed and convenience. A PwC survey shows that 71% of people now prefer multi-channel digital interactions, and 25% want a fully digital banking experience with human support only when necessary.

About Traditional Banks

Traditional banks still play a critical role, no doubt. They’re licensed institutions that handle savings, loans, foreign exchange, and investment services. But the problem is, they’re not keeping up with modern demands. Many banks still rely on physical branches, legacy systems, and bureaucratic processes. That makes them slower to adapt, more expensive to operate, and less inclusive, especially for people in underserved or remote areas.

Case Study: Fintech vs Traditional Banks In Nigeria

Regarding banking in Africa, especially in Nigeria, it feels like fintech and traditional banks are always in a rivalry. But is that the case?

Back in 2018, Nigeria had over 100 fintech companies running mobile money, credit, e-payment, e-collection, and more. At the same time, we still had about 23 commercial banks and a whopping 940 microfinance banks holding down the traditional side. With that many banks, fintech wouldn’t stand a chance, right? But no, that’s not how it played out.

Instead of fighting it out, banks and fintechs started teaming up. Fintechs brought that speed and convenience that customers were craving, while traditional banks kept their trusted reputation and solid customer base. Together, they’re making financial services faster and more accessible, especially for everyday people who just need things to work smoothly.

Here’s where it gets interesting:

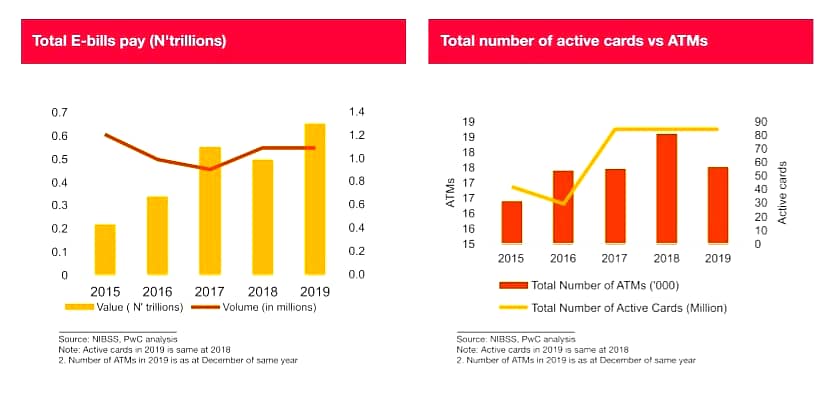

Total active cards in Nigeria stood at more than 84 million by year-end 2019, compared to 29 million cards in 2016. In the same vein, the total number of ATMs and active cards per ATM also increased. As of 2018, an average of one ATM in Nigeria served more than 4,800 active cards. On the other hand, about 0.8 billion transactions valued at N6.5 trillion were processed via ATMs in 2019, relative to 0.9 billion valued at N6.5 trillion in the preceding year.

Meanwhile, mobile channels have emerged to become the most preferred way of making financial transactions in Nigeria. With the rise of affordable smartphones and e-commerce, more and more people now prefer to shop and make payments online using mobile phones. By the end of 2019, the volume of mobile money operations more than quadrupled, while the value processed was about three times that of 2018. Payment for e-bills such as utilities also grew by 40% from N0.5 trillion to about N0.7 trillion in 2019.

What does this tell us? It shows that while ATMs and traditional bank transactions are still significant, mobile money and fintech solutions have rapidly become the go-to for everyday financial needs.

Source: PwC analysis

Who’s Winning In Africa?

Fintech is faster, easier to use, and fits better with the way we live and work now. Whether it’s individuals managing their finances or businesses looking for quicker transactions, fintech is meeting these needs in a way that feels more modern.

However, this doesn’t mean traditional banks are no longer important. They still play a crucial role, particularly in areas like trust and safeguarding people’s money. The real shift is not about fintech replacing banks, but about them working together.

When fintech and traditional banks collaborate, they help make financial services more practical and accessible for everyone. This partnership is driving progress in Africa’s financial sector.

Leave a Reply